Investments, Financial Planning

The investment strategies you chose play a key role in your financial security. Understanding the difference between savings and investing can help you achieve your goals.

1. Don’t Lose Money.

Investments should not lose money. Don’t lose money and you’ll never have to worry about the time it takes to make up for the losses.

2. Cash Flow is Critical.

I believe that keeping your money in a place where it is accessible and still growing is critical. Cash flow is income through liquidity, use and control. When you are in control of your cash flow, it opens the door to a host of opportunities.

3. Never interrupt Compounding.

It takes a skilled person to position their money in such a way that it is continually growing. Consistent growth and annual compounding will outperform erratic and unpredictable speculative risk. One of the most common mistakes Americans make with regard to their finances is the failure to understand the true power of compounding interest. Albert Einstein referred to compounding interest as the eighth wonder of the world. The world has us trained to spend and pay interest rather than save and earn interest. Keeping your money working for you at all times is key. Continuous compounding is part of the miracle.

4. Taxes Matter.

It’s impossible to avoid taxes, but you can and should do everything you can to minimize them. Every dollar of yours that goes to Uncle Sam costs you not just that dollar, but all the dollars you would have made on the interest compounded over time. Paying unnecessary taxes has a significant impact on your financial future. Taxes are the largest single expense you will ever have! Taxes matter and they’ll be going up. It is essential to your financial health to be able to manage tax risk as effectively as possible.

Reduce Your Taxes

If you listen to the financial gurus on TV and Wall Street ‘experts’ you’ll hear a lot about maxing out your 401(k) and IRA contributions in order to get a tax deduction and grow your money tax deferred.

Knowing taxes are likely to be higher in the future, why would you trade in a lower tax rate today for a future rate that could be much higher when you need the money the most? Even if taxes don’t go up, deferring taxes to the future can cost you 3 to 5 times more at withdrawal than you save by getting a tax deduction during your working years.

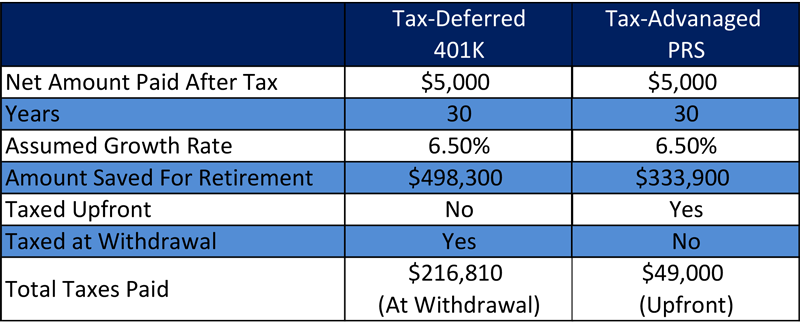

Let’s just look at the math. Here we’ll compare paying your taxes today so you can create tax free retirement cash to deferring your tax bill to sometime in the future:

In this example, let’s say you contribute $5000 per year for 30 years. With a 401(k) you paid no taxes on that money because you got a deduction, on the other side, you would have paid tax at your normal income tax rate, let’s assume 33%.

With the Private Reserve Strategy you would pay $49,500 in taxes ($1650 per year x 30 years).

In this example, when you retire you’ll have $498,300 in the tax-deferred plan or $333,900 in the tax-advantaged PRS.

You’re probably thinking this is a no brainer—I’ll take the tax-deferred plan with the bigger balance. But there is a catch. Let’s say you take out $73,000 a year to live on during retirement. Assuming your money is still growing at 6.5%, you can take $73,000 a year for nine years. However, each year you will have to pay $24,090 in taxes on that money.

That means you could end up paying $216,810 in taxes vs. $49,000 with the tax advantaged Private Reserve Strategy.

And this assumes taxes never go up. It also assumes you never have losses.

Now that you know the truth; how do you feel about paying 3 to 5 times more taxes than you would with a tax-advantaged PRS?